Chapter 17 Regression

17.1 Being satisfied with hospital

A hospital administrator collects data to study the

effect, if any, of a patient’s age, the severity of their

illness, and their anxiety level, on the patient’s satisfaction with

their hospital experience. The data, in the file

link, are

for 46 patients in a survey. The columns are: patient’s satisfaction

score satis, on a scale of 0 to 100; the patient’s age (in

years), the severity of the patient’s illness (also on a

0–100 scale), and the patient’s anxiety score on a standard

anxiety test (scale of 0–5). Higher scores mean greater satisfaction,

increased severity of illness and more anxiety.

- Read in the data and check that you have four columns in your data frame, one for each of your variables.

Solution

This one requires a little thought

first. The data values are aligned in columns, and so are the

column headers. Thus, read_table is what we need:

##

## ── Column specification ─────────────────────────────────────

## cols(

## satis = col_double(),

## age = col_double(),

## severity = col_double(),

## anxiety = col_double()

## )46 rows and 4 columns: satisfaction score (response), age, severity and anxiety (explanatory).

There is a small question about what to call the data

frame. Basically, anything other than satis will do, since

there will be confusion if your data frame has the same name as one of

its columns.

- * Obtain scatterplots of the response variable

satisagainst each of the other variables.

Solution

The obvious way is to do these one after the other:

This is fine, but there is also a way of getting all three plots with

one ggplot. This uses the facet_wrap trick,

but to set that up, we have to have all the \(x\)-variables in

one column, with an extra column labelling which \(x\)-variable

that value was. This uses pivot_longer. The right way to do this is

in a pipeline:

satisf %>%

pivot_longer(-satis, names_to="xname", values_to="x") %>%

ggplot(aes(x = x, y = satis)) + geom_point() +

facet_wrap(~xname, scales = "free", ncol = 2)

Steps: collect together the columns age through anxiety into one column

whose values go in x, with names in xname, then plot this new

x against satisfaction score, with a separate facet for each

different \(x\) (in xname).

What’s the difference

between facet_grid and facet_wrap? The difference is that with

facet_wrap, we are letting ggplot arrange the

facets how it wants to. In this case, we didn’t care which explanatory

variable went on which facet, just as long as we saw all of them

somewhere. Inside facet_wrap there are no dots: a

squiggle, followed by the name(s) of the variable(s) that

distinguish(es) the facets.

If there are more than one, they should be separated by plus signs as in lm. Each facet then has as many labels as variables. I haven’t actually done this myself, but from looking at examples, I think this is the way it works.

The only “design” decision I made here was that the facets

should be arranged somehow in two columns, but I didn’t care which

ones should be where.

In facet_grid, you have a variable that you want to be

displayed in rows or in columns (not just in “different facets”).

I’ll show you how that works here. Since I am going to draw

two plots, I should save the long data frame first and re-use it,

rather than calculating it twice (so that I ought now to go back and

do the other one using the saved data frame, really):

If, at this or any stage, you get confused, the way to un-confuse yourself is to fire up R Studio and do this yourself. You have all the data and code you need. If you do it yourself, you can run pipes one line at a time, inspect things, and so on.

First, making a row of plots, so that xname is the \(x\)

of the facets:

I find these too tall and skinny to see the trends, as on the first

facet_wrap plot.

And now, making a column of plots, with xname as \(y\):

This one looks weird because the three \(x\)-variables are on different

scales. The effect of the scales="free" is to allow the

satis scale to vary, but the x scale cannot because

the facets are all in a line. Compare this:

ggplot(satisf.long, aes(x = x, y = satis)) + geom_point() +

facet_wrap(~xname, ncol = 1, scales = "free")

This time, the \(x\) scales came out different (and suitable), but I still like squarer plots better for judging relationships.

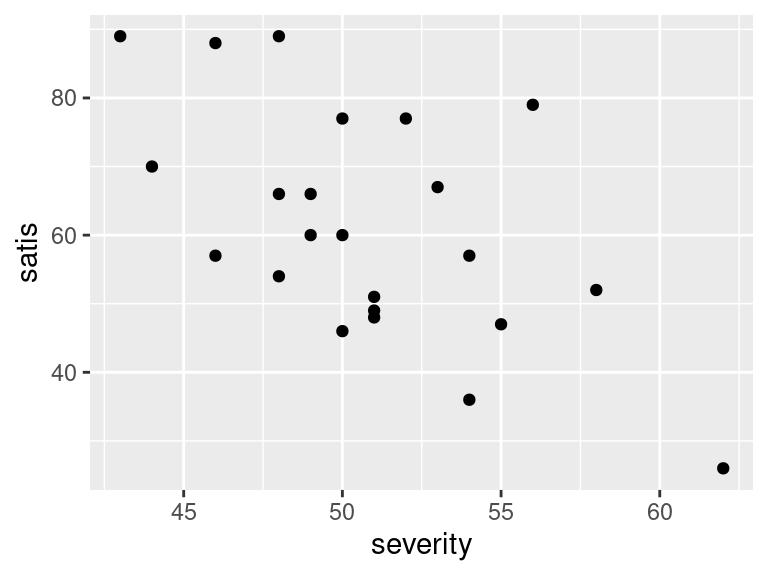

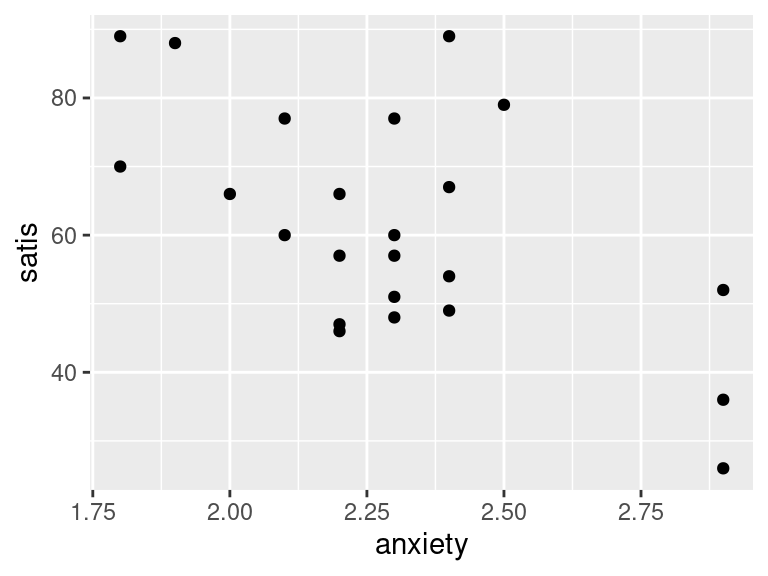

- In your scatterplots of (here), which relationship appears to be the strongest one?

Solution

All the trends appear to be downward ones, but

I think satis and age is the strongest

trend. The other ones look more scattered to me.

- * Create a correlation matrix for all four variables. Does your strongest trend of the previous part have the strongest correlation?

Solution

This is a matter of running the whole data frame through cor:

## satis age severity anxiety

## satis 1.0000000 -0.7736828 -0.5874444 -0.6023105

## age -0.7736828 1.0000000 0.4666091 0.4976945

## severity -0.5874444 0.4666091 1.0000000 0.7945275

## anxiety -0.6023105 0.4976945 0.7945275 1.0000000Ignoring the correlations of variables with themselves, the

correlation of satisf with age, the one I picked

out, is the strongest (the most negative trend). If you picked one of

the other trends as the strongest, you need to note how close it is to

the maximum correlation: for example, if you picked satis

and severity, that’s the second highest correlation (in

size).

- Run a regression predicting satisfaction from the other three variables, and display the output.

Solution

##

## Call:

## lm(formula = satis ~ age + severity + anxiety, data = satisf)

##

## Residuals:

## Min 1Q Median 3Q Max

## -16.954 -7.154 1.550 6.599 14.888

##

## Coefficients:

## Estimate Std. Error t value Pr(>|t|)

## (Intercept) 162.8759 25.7757 6.319 4.59e-06 ***

## age -1.2103 0.3015 -4.015 0.00074 ***

## severity -0.6659 0.8210 -0.811 0.42736

## anxiety -8.6130 12.2413 -0.704 0.49021

## ---

## Signif. codes:

## 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

##

## Residual standard error: 10.29 on 19 degrees of freedom

## Multiple R-squared: 0.6727, Adjusted R-squared: 0.621

## F-statistic: 13.01 on 3 and 19 DF, p-value: 7.482e-05- Does the regression fit well overall? How can you tell?

Solution

For this, look at R-squared, which is 0.682 (68.2%). This is one of those things to have an opinion about. I’d say this is good but not great. I would not call it “poor”, since there definitely is a relationship, even if it’s not a stupendously good one.

- Test the null hypothesis that none of your explanatory variables help, against the alternative that one or more of them do. (You’ll need an appropriate P-value. Which one is it?) What do you conclude?

Solution

This one is the (global) \(F\)-test, whose P-value is at the

bottom. It translates to 0.000000000154, so this is

definitely small, and we reject the null. Thus, one or more

of age, severity and anxiety helps to

predict satisfaction. (I would like to see this last sentence,

rather than just “reject the null”.)

- The correlation between

severityandsatisis not small, but in my regression I found thatseveritywas nowhere near significant. Why is this? Explain briefly.

Solution

The key thing to observe is that the \(t\)-test in the regression

says how important a variable is , or, if you prefer, how much that

variable adds to the regression, on top of the ones that

are already there. So here, we are saying

that severity has nothing to add, given that the

regression already includes the others. (That is, high correlation

and strong significance don’t always go together.)

For a little more insight, look at the correlation matrix of

(here) again. The strongest trend with

satis is with age, and indeed age is

the one obviously significant variable in the regression. The

trend of severity with satis is somewhat

downward, and you might otherwise have guessed that this is strong

enough to be significant. But see that severity

also has a clear relationship with age. A patient

with low severity of disease is probably also younger, and we know

that younger patients are likely to be more satisfied. Thus

severity has nothing (much) to add.

The multiple regression is actually doing something clever

here. Just looking at the correlations, it appears that all three

variables are helpful, but the regression is saying that once you

have looked at age (“controlled for age”),

severity of illness does not have an impact: the correlation of

severity with satis is as big as it is almost

entirely because of age.

This gets into the domain of “partial correlation”. If you like videos, you can

see link for

this. I prefer regression, myself, since I find it clearer.

anxiety

tells a different story: this is close to significant (or

is significant at the \(\alpha=0.10\) level), so the

regression is saying that anxiety does appear to

have something to say about satis over and above

age. This is rather odd, to my mind, since

anxiety has only a slightly stronger correlation with

satis and about the same with age as

severity does. But the regression is telling the story to

believe, because it handles all the inter-correlations, not just

the ones between pairs of variables.

I thought it would be rather interesting to do some predictions

here. Let’s predict satisfaction for all combinations of high and

low age, severity and anxiety. I’ll use the quartiles for high and

low. There is a straightforward but ugly way:

quartiles <- satisf %>% summarize(

age_q1 = quantile(age, 0.25),

age_q3 = quantile(age, 0.75),

severity_q1 = quantile(severity, 0.25),

severity_q3 = quantile(severity, 0.75),

anxiety_q1 = quantile(anxiety, 0.25),

anxiety_q3 = quantile(anxiety, 0.75)

)This is ugly because of all the repetition (same quantiles of different variables), and the programmer in you should be offended by the ugliness. Anyway, it gives what we want:

You can copy the numbers from here to below, or you can do some cleverness to get them in the right places:

quartiles %>%

pivot_longer(everything(), names_to="var_q", values_to="quartile") %>%

separate(var_q, c("var_name", "which_q")) %>%

pivot_wider(names_from=var_name, values_from=quartile)This combo of pivot_longer and separate can be shortened further by specifying two names in names_to, and also specifying a names_sep to say what they’re separated by:

quartiles %>%

pivot_longer(everything(), names_to=c("var_q", "which_q"),

names_sep="_", values_to="quartile") %>%

pivot_wider(names_from=var_q, values_from=quartile)Believe it or not, this can be shortened even further, thus:

The place where this approach gains is when pivot_longer goes too far, making everything longer, when you want some of it to be wider and thus you needed a pivot_wider at the end. Once again, you use two things in the names_to, but this time instead of giving both variables names, you use the special name .value for the thing you want to end up in columns. The original data frame quartiles had columns with names like severity_q1, so here that is the first thing: age and severity and anxiety will be used as column names, and filled automatically with the values for q1 and q3, so you don’t specify a values_to.

This is one of those very dense pieces of coding, where you accomplish a lot in a small space. If it is too dense for you, you can go back to one of the two previous ways of doing it, eg. the simple pivot_longer followed by separate followed by pivot_wider. Sometimes there is value in using a larger number of simpler tools to get where you want.

Those data frames above are we want for below. Let’s test the first way of coding it line by line to see exactly what it did: (The second way does the first two lines in one, and the third way does all three.)

Making longer. everything() is a select-helper saying

“pivot-longer all the columns”.

quartiles %>%

pivot_longer(everything(), names_to="var_q", values_to="quartile") %>%

separate(var_q, c("var_name", "which_q")) The column var_q above encodes a variable and a

quartile, so split them up. By default, separate splits at an

underscore, which is why the things in quartiles were named

with underscores.

I’d like to claim that I was clever enough to think of this in advance, but I wasn’t; originally the variable name and the quartile name were separated by dots, which made the separate more complicated, so I went back and changed it.

Now put the variable names back in the columns:

quartiles %>%

pivot_longer(everything(), names_to="var_q", values_to="quartile") %>%

separate(var_q, c("var_name", "which_q")) %>%

pivot_wider(names_from=var_name, values_from=quartile) -> qq

qqI make var_name wider, carrying along the values in

quartile (which means that the rows will get matched up by

which_q).

Now, let’s think about why we were doing that. We want to do

predictions of all possible combinations of those values of age and

anxiety and severity.

Doing “all possible combinations” calls for crossing,

which looks like this. It uses the output from one of the above pipelines, which I saved in qq:

There are two possibilities for each variable, so there are \(2^3=8\)

“all possible combinations”. You can check that crossing got

them all.

This is a data frame containing all the values we want to predict for,

with columns having names that are the same as the variables in the

regression, so it’s ready to go into predict. I’ll do

prediction intervals, just because:

Looking at the predictions themselves (in fit), you can see

that age has a huge effect. If you compare the 1st and 5th

lines (or the 2nd and 6th, 3rd and 7th, ) you see that

increasing age by 13.5 years, while leaving the other variables the

same, decreases the satisfaction score by over 15 on

average. Changing severity, while leaving everything else the

same, has in comparison a tiny effect, just over 2 points. (Compare

eg. 1st and 2nd lines.) Anxiety has an in-between effect: increasing

anxiety from 2.1 to 2.475, leaving everything else fixed, decreases

satisfaction by about 5 points on average.

I chose the quartiles on purpose: to demonstrate the change in average

satisfaction by changing the explanatory variable by an appreciable

fraction of its range of values. That is, I changed severity

by “a fair bit”, and still the effect on satisfaction scores was small.

Are any of these prediction intervals longer or shorter? We can calculate how long they are. Look at the predictions:

## fit lwr upr

## 1 72.45391 50.11023 94.79759

## 2 68.79143 45.11580 92.46706

## 3 70.30065 46.84885 93.75246

## 4 66.63817 43.77908 89.49727

## 5 58.53525 35.87346 81.19705

## 6 54.87277 31.28639 78.45915

## 7 56.38200 33.09400 79.66999

## 8 52.71951 30.44067 74.99836This is unfortunately not a data frame:

## [1] "matrix" "array"so we make it one before calculating the lengths.

We want upr minus lwr:

Now, I don’t want to keep the other stuff from pp, so I used

transmute instead of mutate; transmute

keeps only the new variable(s) that I calculate and throws away

the others.

Usually you want to keep the other variables around as well, which is why you don’t see transmute very often.

Then I put that side by side with the values being predicted for:

pp %>%

as_tibble() %>%

transmute(pi.length = upr - lwr) %>%

bind_cols(satisf.new) %>%

arrange(pi.length)Two of these are noticeably shorter than the others. These are high-everything and low-everything. If you look back at the scatterplot matrix of (here), you’ll see that the explanatory variables have positive correlations with each other. This means that when one of them is low, the other ones will tend to be low as well (and correspondingly high with high). That is, most of the data is at or near the low-low-low end or the high-high-high end, and so those values will be easiest to predict for.

I was actually expecting more of an effect, but what I expected is actually there.

In the backward elimination part (coming up), I found that only

age and anxiety had a significant impact on

satisfaction, so I can plot these two explanatory variables against

each other to see where most of the values are:

There is basically no data with low age and high anxiety, or with high age and low anxiety, so these combinations will be difficult to predict satisfaction for (and thus their prediction intervals will be longer).

- Carry out a backward elimination to determine which of

age,severityandanxietyare needed to predict satisfaction. What do you get?

Solution

This means starting with the regression containing all the explanatory

variables, which is the one I called satisf.1:

##

## Call:

## lm(formula = satis ~ age + severity + anxiety, data = satisf)

##

## Residuals:

## Min 1Q Median 3Q Max

## -16.954 -7.154 1.550 6.599 14.888

##

## Coefficients:

## Estimate Std. Error t value Pr(>|t|)

## (Intercept) 162.8759 25.7757 6.319 4.59e-06 ***

## age -1.2103 0.3015 -4.015 0.00074 ***

## severity -0.6659 0.8210 -0.811 0.42736

## anxiety -8.6130 12.2413 -0.704 0.49021

## ---

## Signif. codes:

## 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

##

## Residual standard error: 10.29 on 19 degrees of freedom

## Multiple R-squared: 0.6727, Adjusted R-squared: 0.621

## F-statistic: 13.01 on 3 and 19 DF, p-value: 7.482e-05Pull out the least-significant (highest P-value) variable, which here

is severity. We already decided that this had nothing to add:

##

## Call:

## lm(formula = satis ~ age + anxiety, data = satisf)

##

## Residuals:

## Min 1Q Median 3Q Max

## -17.868 -6.649 2.506 6.445 16.120

##

## Coefficients:

## Estimate Std. Error t value Pr(>|t|)

## (Intercept) 147.0751 16.7334 8.789 2.64e-08 ***

## age -1.2434 0.2961 -4.199 0.000442 ***

## anxiety -15.8906 8.2556 -1.925 0.068593 .

## ---

## Signif. codes:

## 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

##

## Residual standard error: 10.2 on 20 degrees of freedom

## Multiple R-squared: 0.6613, Adjusted R-squared: 0.6275

## F-statistic: 19.53 on 2 and 20 DF, p-value: 1.985e-05If you like, copy and paste the first lm, edit it to get rid

of severity, and run it again. But when I have a

“small change” to make to a model, I like to use update.

Having taken severity out, anxiety has become

strongly significant. Since all of the explanatory variables are now

significant, this is where we stop. If we’re predicting satisfaction,

we need to know both a patient’s age and their anxiety score: being

older or more anxious is associated with a decrease in satisfaction.

There is also a function step that will do this for you:

## Start: AIC=110.84

## satis ~ age + severity + anxiety

##

## Df Sum of Sq RSS AIC F value Pr(>F)

## - anxiety 1 52.41 2064.0 109.43 0.4951 0.4902110

## - severity 1 69.65 2081.2 109.62 0.6579 0.4273559

## <none> 2011.6 110.84

## - age 1 1706.67 3718.3 122.97 16.1200 0.0007404 ***

## ---

## Signif. codes:

## 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

##

## Step: AIC=109.43

## satis ~ age + severity

##

## Df Sum of Sq RSS AIC F value Pr(>F)

## <none> 2064.0 109.43

## - severity 1 402.78 2466.8 111.53 3.9029 0.0621629 .

## - age 1 1960.56 4024.6 122.79 18.9977 0.0003042 ***

## ---

## Signif. codes:

## 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1##

## Call:

## lm(formula = satis ~ age + severity, data = satisf)

##

## Coefficients:

## (Intercept) age severity

## 166.591 -1.260 -1.089with the same result. This function doesn’t actually use P-values;

instead it uses a thing called AIC. At each step, the variable with

the lowest AIC comes out, and when <none> bubbles up to the

top, that’s when you stop. The test="F" means

“include an \(F\)-test”, but the procedure still uses AIC (it just shows you an

\(F\)-test each time as well). In this case, the other variables were

in the same order throughout, but they don’t have to be (in the same

way that removing one variable from a multiple regression can

dramatically change the P-values of the ones that remain). Here, at

the first step, <none> and anxiety were pretty

close, but when severity came out, taking out nothing was a

lot better than taking out anxiety.

The test="F" on the end gets you the P-values. Using the

\(F\)-test is right for regressions; for things like logistic regression

that we see later, test="Chisq" is the right one to

use.

This is F in quotes, meaning F-test, not F without quotes, meaning FALSE.

17.2 Handling shipments of chemicals

The data in link are on shipments of chemicals in drums that arrive at a warehouse. In order, the variables are:

the number of minutes required to handle the shipment

the number of drums in the shipment

the total weight of the shipment, in hundreds of pounds.

- The data set has two features: no column names, and data aligned in columns (that is, more than one space between data values). Read the data in, giving the columns suitable names. To do this, you may have to consult an appropriate help file, or do some searching, perhaps of one of the other questions on this assignment.

Solution

The alignment of columns means that we need to use

read_table. Once you’ve figured that out, you can

search for help by typing ?read_table in the Console

window (the help will appear bottom right), or you can put the

same thing into an R Notebook code chunk, and when you run the

chunk, the help will be displayed. (Press control-shift-1 to go

back to the notebook.)

Or you can Google it, of course.

The key observation is that you need to supply some column names

in col_names, like this:

my_url <- "http://statweb.lsu.edu/EXSTWeb/StatLab/DataSets/NKNWData/CH06PR09.txt"

cols <- c("minutes", "drums", "weight")

chemicals <- read_table(my_url, col_names = cols)##

## ── Column specification ─────────────────────────────────────

## cols(

## minutes = col_double(),

## drums = col_double(),

## weight = col_double()

## )I like to define my URL and column names up front. You can define

either of them in the read_table, but it makes that line

longer. Up to you.

There is no skip here, because the data file starts right

away with the data and we want to use all the values: we are

adding names to what’s in the data file. If you used

skip, you will be one observation short all the way through,

and your output will be slightly different from mine all the way

through.

Use any names you like, but they should resemble what the columns actually represent.

- Fit a regression predicting the number of minutes required to handle a shipment from the other two variables. Display the results.

Solution

##

## Call:

## lm(formula = minutes ~ drums + weight, data = chemicals)

##

## Residuals:

## Min 1Q Median 3Q Max

## -8.8353 -3.5591 -0.0533 2.4018 15.1515

##

## Coefficients:

## Estimate Std. Error t value Pr(>|t|)

## (Intercept) 3.3243 3.1108 1.069 0.3

## drums 3.7681 0.6142 6.135 1.10e-05 ***

## weight 5.0796 0.6655 7.632 6.89e-07 ***

## ---

## Signif. codes:

## 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

##

## Residual standard error: 5.618 on 17 degrees of freedom

## Multiple R-squared: 0.9869, Adjusted R-squared: 0.9854

## F-statistic: 641.6 on 2 and 17 DF, p-value: < 2.2e-16- Explain carefully but briefly what the slope coefficients for the two explanatory variables represent. Do their signs (positive or negative) make practical sense in the context of handling shipments of chemicals?

Solution

The slope coefficient for drums is 3.77; this means that

a shipment with one extra drum (but the same total weight) would

take on average 3.77 minutes longer to handle. Likewise, the slope

coefficient for weight is 5.08, so a shipment that

weighs 1 hundred more pounds but has the same number of drums

will take 5.08 more minutes to handle.

Or “each additional drum, all else equal, will take 3.77 more minutes to handle”, or similar wording. You have to get at two

things: a one-unit increase in the explanatory variable going with

a certain increase in the response, and also the “all else equal” part. How you say it is up to you, but you need to say it.

That was two marks. The third one comes from noting that both

slope coefficients are positive, so making a shipment either

contain more drums or weigh more makes the handling time longer as

well. This makes perfect sense, since either kind of increase

would make the shipment more difficult to handle, and thus take

longer.

I was not asking about P-values. There isn’t really much to

say about those: they’re both significant, so the handling time

depends on both the total weight and the number of drums. Removing

either from the regression would be a mistake.

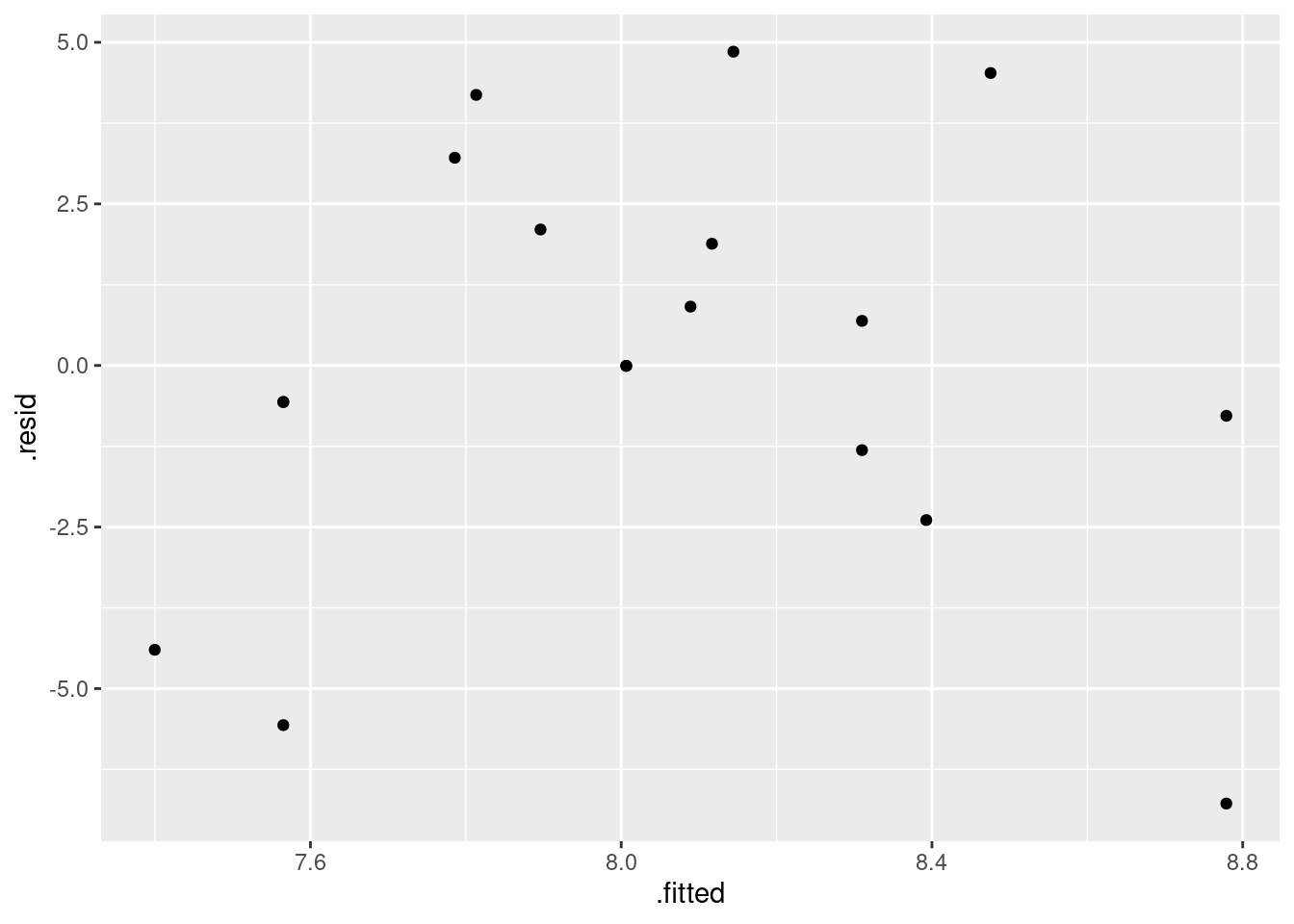

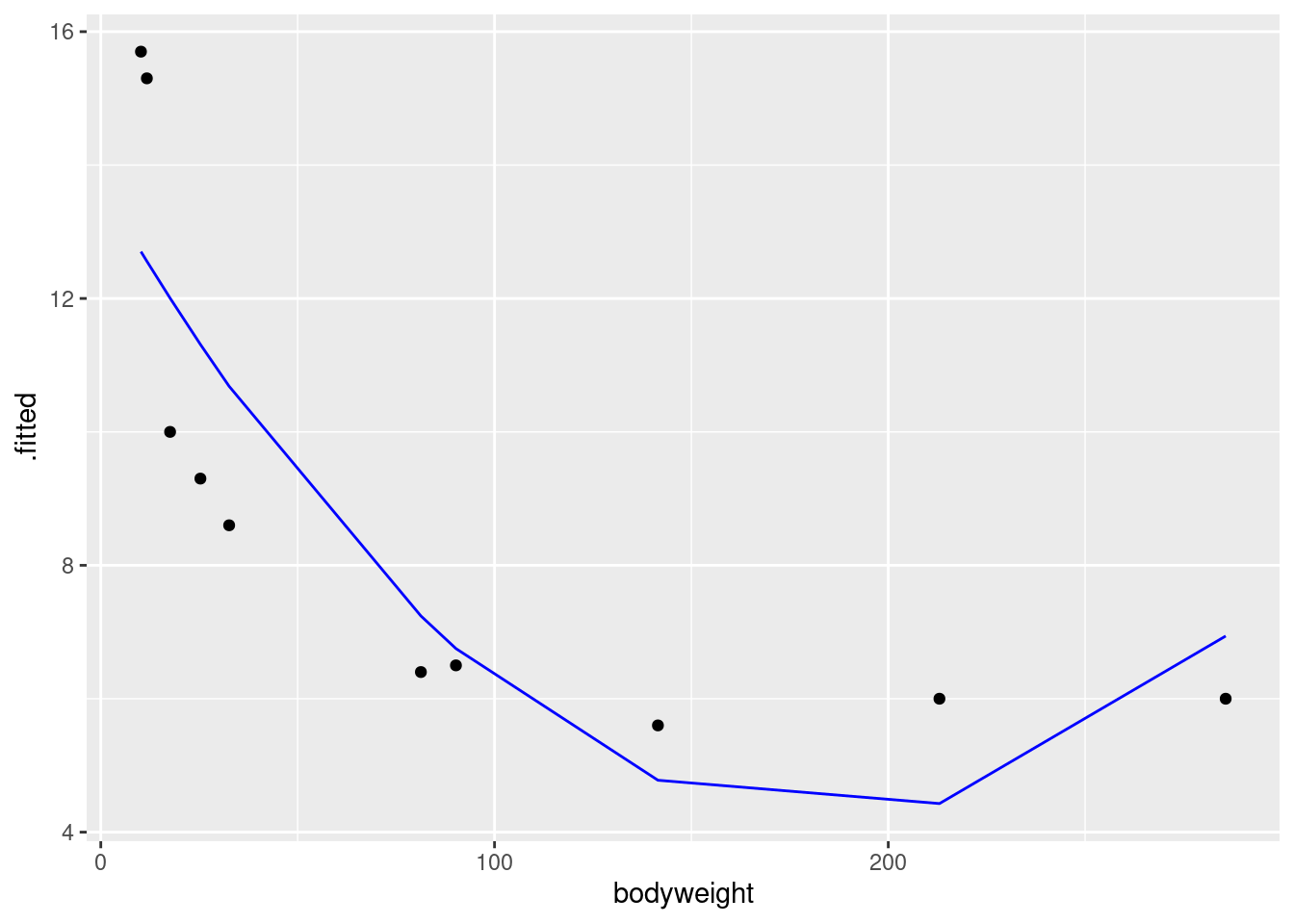

- Obtain plots of residuals against fitted values, residuals against explanatory variables, and a normal quantile plot of the residuals.

Solution

These are the standard plots from a multiple regression. The second one requires care, but the first and last should be straightforward. Residuals against fitted values:

The tricky part about the second one is that the \(x\)-values and the

residuals come from different data frames, which has to get expressed

in the ggplot. The obvious way is to do the two plots (one

for each explanatory variable) one at a time:

and

What would also work is to make a data frame first with the things to plot:

and then:

and similarly for drums. The resid with the model

name in brackets seems to be necessary.

Another way to approach this is augment from

broom. That does this:

and then you can use d as the “base” data frame from which

everything comes:

and

or you can even do that trick to put the two plots on facets:

d %>%

pivot_longer(drums:weight, names_to="xname", values_to="x") %>%

ggplot(aes(x = x, y = .resid)) + geom_point() +

facet_wrap(~xname)

Last, the normal quantile plot:

As a check for the grader, there should be four plots, obtained

somehow: residuals against fitted values, normal quantile plot of

residuals, residuals against drums, residuals against

weight.

- Do you have any concerns, looking at the residual plots? Explain briefly.

Solution

The (only) concern I have, looking at those four plots, is the one very positive residual, the one around 15. Take that away, and I think all of the plots are then acceptable. Alternatively, I will take something like “I have no concerns about the form of the relationship”, saying that the kind of model being fitted here is OK (no evidence of non-linearity, fanning out, that kind of stuff). It’s up to you to decide whether you think “concerns” extends to outliers, high-influence points, etc. The normal quantile plot reveals that the most negative residual, the one around \(-9\), is in fact almost exactly as negative as you would expect the most negative residual to be, so it is not an outlier at all. The residuals are almost exactly normally distributed, except for the most positive one. I don’t think you can justify fanning-in, since the evidence for that is mostly from the single point on the right. The other points do not really have residuals closer to zero as you move left to right.

Do not be tempted to pick out everything you can think of wrong with these plots. The grader can, and will, take away points if you start naming things that are not concerns.

Extra: what else can I find out about that large-positive-residual point? This is where having the “augmented” data frame is a plus:

As shown. The predicted number of minutes is 96.8, but the actual

number of minutes it took is 112. Hence the residual of 15.2.

Can we find “similar” numbers of drums and

weight and compare the minutes? Try this:

You might not have seen between before, but it works the way

you’d expect.

weight between 8 and 11, for example, returning TRUE or FALSE. Two other shipments with similar numbers of drums and

total weight took around 90–100 minutes to handle, so the 112 does

look about 15 minutes too long. This was actually an average-sized shipment:

library(ggrepel)

d %>%

mutate(my_label = ifelse(.resid > 10, "residual +", "")) %>%

ggplot(aes(x = drums, y = weight, colour = minutes, label = my_label)) +

geom_point() + geom_text_repel()

so it’s a bit of a mystery why it took so long to handle.

I had some fun with the graph: if you set colour equal to a

continuous variable (as minutes is here), you get a

continuous colour scale, by default from dark blue (small) to light

blue (large). The number of minutes tends to get larger (lighter) as

you go up and to the right with bigger shipments. The point labelled

“residual +” is the one with the large residual; it is a

noticeably lighter blue than the points around it, meaning that it

took longer to handle than those points. I used the trick from C32 to

label “some” (here one) of the points: create a new label variable

with a mutate and an ifelse, leaving all of the

other labels blank so you don’t see them.

The blue colour scheme is a little hard to judge values on. Here’s another way to do that:

d %>%

mutate(my_label = ifelse(.resid > 10, "residual +", "")) %>%

ggplot(aes(x = drums, y = weight, colour = minutes, label = my_label)) +

geom_point() + geom_text_repel() +

scale_colour_gradient(low = "red", high = "blue")

The labelled point is a little more blue (purplish) than the more clearly red points near it.

The other thing to see is that there is also a positive correlation

between the number of drums and the total weight, which is what you’d

expect. Unlike with some of our other examples, this wasn’t strong

enough to cause problems; the separate effects of drums and

weight on minutes were distinguishable enough to

allow both explanatory variables to have a strongly significant effect

on minutes.

Post scriptum: the “drums” here are not concert-band-type drums, but something like this:

17.3 Salaries of mathematicians

A researcher in a scientific foundation wanted to evaluate the relationship between annual salaries of mathematicians and three explanatory variables:

an index of work quality

number of years of experience

an index of publication success.

The data can be found at link. Data from only a relatively small number of mathematicians were available.

- Read in the data and check that you have a sensible number of rows and the right number of columns. (What does “a sensible number of rows” mean here?)

Solution

This is a tricky one. There are aligned columns, but the column headers are not aligned with them.

Thus read_table2 is what you need.

##

## ── Column specification ─────────────────────────────────────

## cols(

## salary = col_double(),

## workqual = col_double(),

## experience = col_double(),

## pubsucc = col_double()

## )24 observations (“only a relatively small number”) and 4 columns, one for the response and one each for the explanatory variables.

Or, if you like,

## [1] 24 4for the second part: 24 rows and 4 columns again. I note, with only 24 observations, that we don’t really have enough data to investigate the effects of three explanatory variables, but we’ll do the best we can. If the pattern, whatever it is, is clear enough, we should be OK.

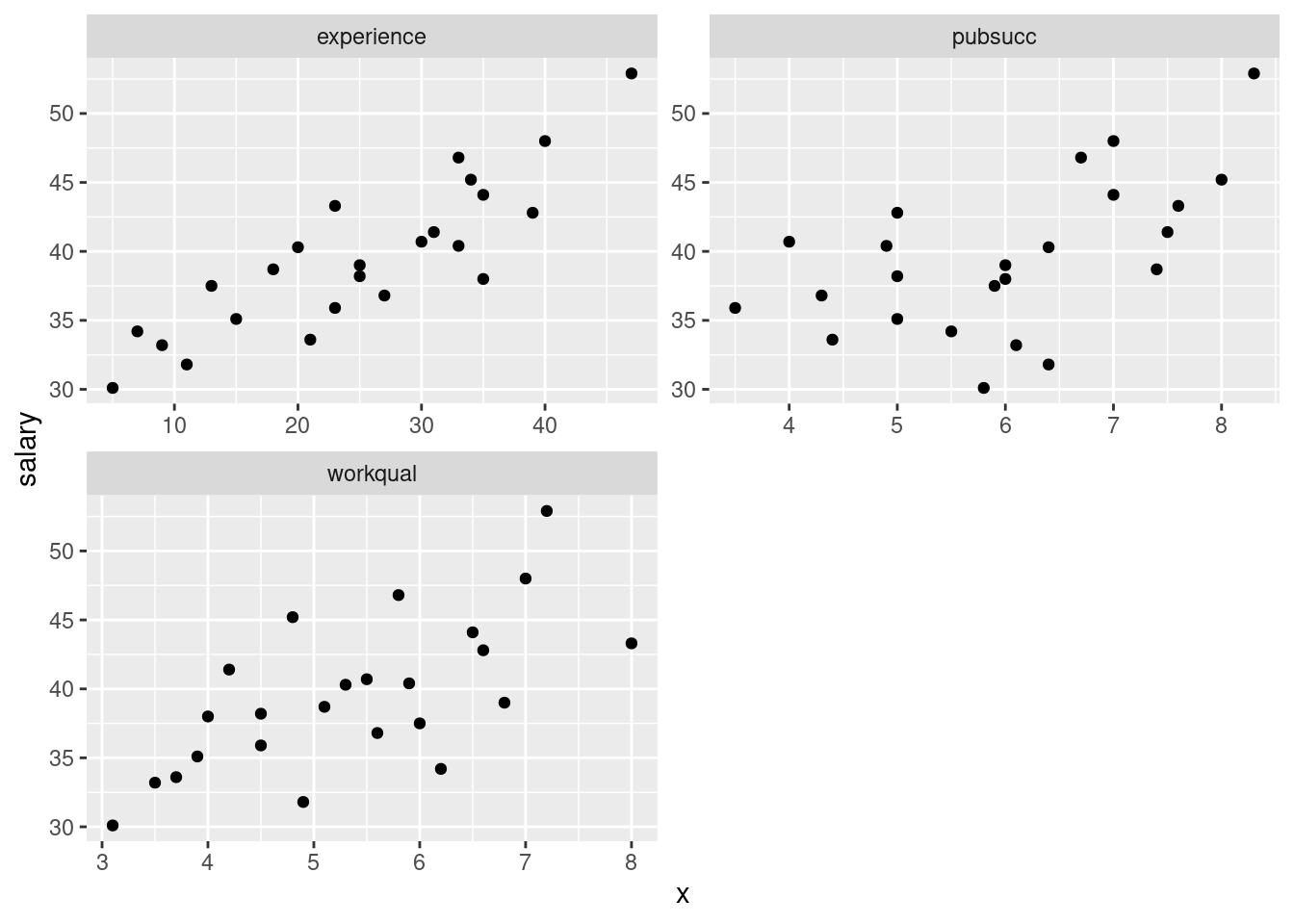

- Make scatterplots of

salaryagainst each of the three explanatory variables. If you can, do this with oneggplot.

Solution

The obvious way to do this is as three separate scatterplots, and that will definitely work. But you can do it in one go if you think about facets, and about having all the \(x\)-values in one column (and the names of the \(x\)-variables in another column):

salaries %>%

pivot_longer(-salary, names_to="xname", values_to="x") %>%

ggplot(aes(x = x, y = salary)) + geom_point() +

facet_wrap(~xname, ncol = 2, scales = "free")

If you don’t see how that works, run it yourself, one line at a time.

I was thinking ahead a bit while I was coding that: I wanted the three

plots to come out about square, and I wanted the plots to have their

own scales. The last thing in the facet_wrap does the latter,

and arranging the plots in two columns (thinking of the plots as a set

of four with one missing) gets them more or less square.

If you don’t think of those, try it without, and then fix up what you don’t like.

- Comment briefly on the direction and strength of each

relationship with

salary.

Solution

To my mind, all of the three relationships are going uphill (that’s the “direction” part). experience is the

strongest, and pubsucc looks the weakest (that’s the

“strength” part). If you want to say there is no relationship

with pubsucc, that’s fine too. This is a judgement

call.

Note that all the relationships are more or less linear (no

obvious curves here). We could also investigate the relationships

among the explanatory variables:

## salary workqual experience pubsucc

## salary 1.0000000 0.6670958 0.8585582 0.5581960

## workqual 0.6670958 1.0000000 0.4669511 0.3227612

## experience 0.8585582 0.4669511 1.0000000 0.2537530

## pubsucc 0.5581960 0.3227612 0.2537530 1.0000000Mentally cut off the first row and column (salary is the

response). None of the remaining correlations are all that high, so we

ought not to have any multicollinearity problems.

- * Fit a regression predicting salary from the other three

variables, and obtain a

summaryof the results.

Solution

##

## Call:

## lm(formula = salary ~ workqual + experience + pubsucc, data = salaries)

##

## Residuals:

## Min 1Q Median 3Q Max

## -3.2463 -0.9593 0.0377 1.1995 3.3089

##

## Coefficients:

## Estimate Std. Error t value Pr(>|t|)

## (Intercept) 17.84693 2.00188 8.915 2.10e-08 ***

## workqual 1.10313 0.32957 3.347 0.003209 **

## experience 0.32152 0.03711 8.664 3.33e-08 ***

## pubsucc 1.28894 0.29848 4.318 0.000334 ***

## ---

## Signif. codes:

## 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

##

## Residual standard error: 1.753 on 20 degrees of freedom

## Multiple R-squared: 0.9109, Adjusted R-squared: 0.8975

## F-statistic: 68.12 on 3 and 20 DF, p-value: 1.124e-10- How can we justify the statement “one or more of the explanatory variables helps to predict salary”? How is this consistent with the value of R-squared?

Solution

“One or more of the explanatory variables helps” is an invitation to consider the (global) \(F\)-test for the whole regression. This has the very small P-value of \(1.124\times 10^{-10}\) (from the bottom line of the output): very small, so one or more of the explanatory variables does help, and the statement is correct. The idea that something helps to predict salary suggests (especially with such a small number of observations) that we should have a high R-squared. In this case, R-squared is 0.9109, which is indeed high.

- Would you consider removing any of the variables from this regression? Why, or why not?

Solution

Look at the P-values attached to each variable. These are all

very small: 0.003, 0.00000003 and 0.0003, way smaller than

0.05. So it would be a mistake to

take any, even one, of the variables out: doing so would make the

regression much worse.

If you need convincing of that, see what happens when we take

the variable with the highest P-value out — this is workqual:

##

## Call:

## lm(formula = salary ~ experience + pubsucc, data = salaries)

##

## Residuals:

## Min 1Q Median 3Q Max

## -5.2723 -0.7865 -0.3983 1.7277 3.2060

##

## Coefficients:

## Estimate Std. Error t value Pr(>|t|)

## (Intercept) 21.02546 2.14819 9.788 2.82e-09 ***

## experience 0.37376 0.04104 9.107 9.70e-09 ***

## pubsucc 1.52753 0.35331 4.324 3e-04 ***

## ---

## Signif. codes:

## 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

##

## Residual standard error: 2.137 on 21 degrees of freedom

## Multiple R-squared: 0.8609, Adjusted R-squared: 0.8477

## F-statistic: 65 on 2 and 21 DF, p-value: 1.01e-09R-squared has gone down from 91% to 86%: maybe not so much in the

grand scheme of things, but it is noticeably less. Perhaps better,

since we are comparing models with different numbers of explanatory

variables, is to compare the adjusted R-squared: this has gone

down from 90% to 85%. The fact that this has gone down at all

is enough to say that taking out workqual was a

mistake.

Adjusted R-squareds are easier to compare in this context, since you don’t have to make a judgement about whether it has changed substantially, whatever you think substantially means.

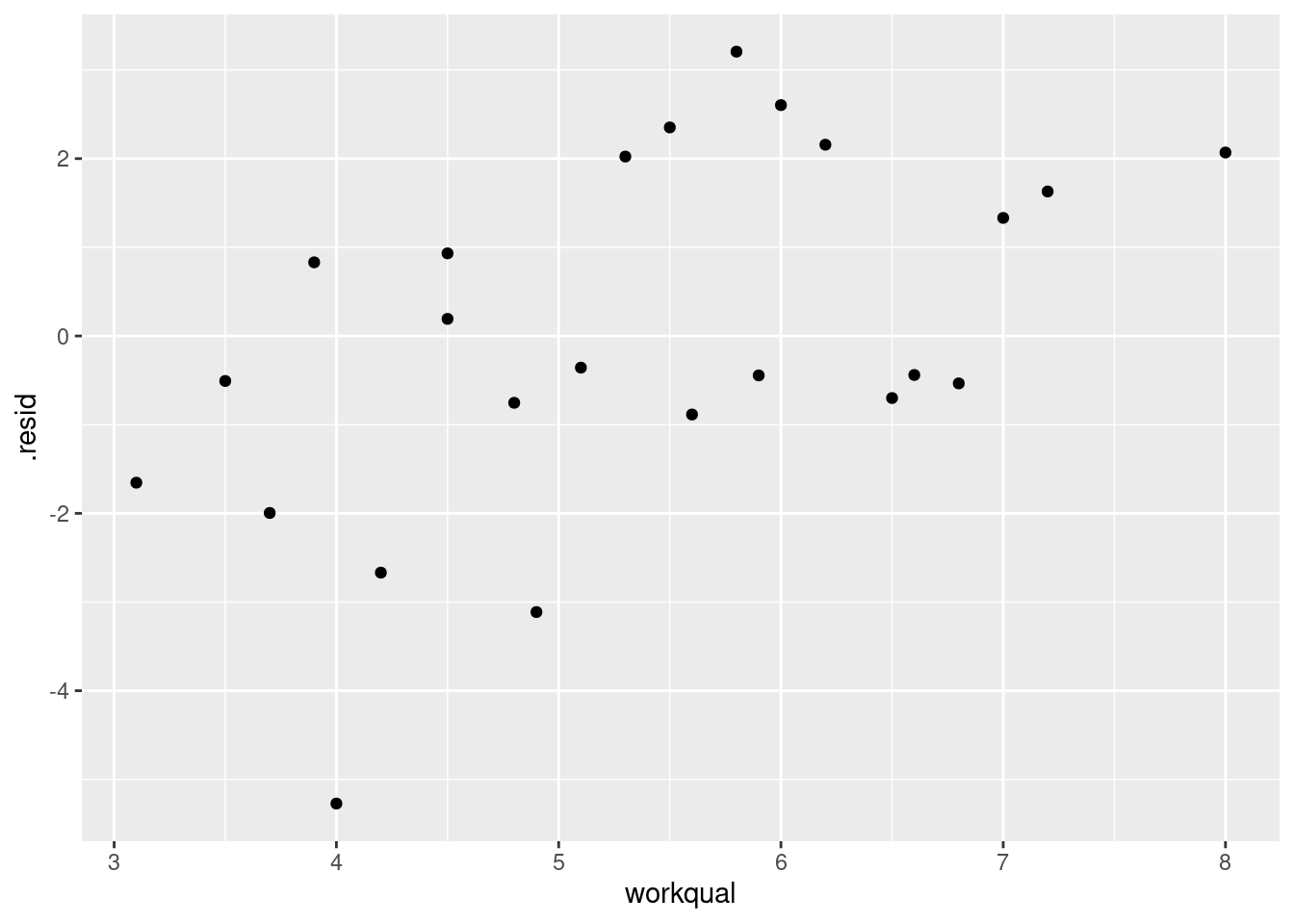

Another way of seeing whether a variable has anything to add in a

regression containing the others is a partial regression plot.

We take the residuals from salaries.2 above and plot

them against the variable we removed, namely

workqual.

The residuals have to be the ones from a regression not including the \(x\)-variable you’re testing. If

workqual has nothing to add, there will be no pattern; if it

does have something to add, there will be a trend. Like

this. I use augment from broom:

library(broom)

salaries.2 %>%

augment(salaries) %>%

ggplot(aes(x = workqual, y = .resid)) + geom_point()

This is a mostly straight upward trend. So we

need to add a linear term in workqual to the

regression.

Or not take it out in the first place.

- Do you think it would be a mistake to take both of

workqualandpubsuccout of the regression? Do a suitable test. Was your guess right?

Solution

I think it would be a big mistake. Taking even one of these variables out of the regression is a bad idea (from the \(t\)-tests), so taking out more than one would be a really bad idea. To perform a test, fit the model without these two explanatory variables:

and then use anova to compare the two regressions, smaller

model first:

The P-value is extremely small, so the bigger model is definitely better than the smaller one: we really do need all three variables. Which is what we guessed.

- Back in part (here), you fitted a regression with all three explanatory variables. By making suitable plots, assess whether there is any evidence that (i) that the linear model should be a curve, (ii) that the residuals are not normally distributed, (iii) that there is “fan-out”, where the residuals are getting bigger in size as the fitted values get bigger? Explain briefly how you came to your conclusions in each case.

Solution

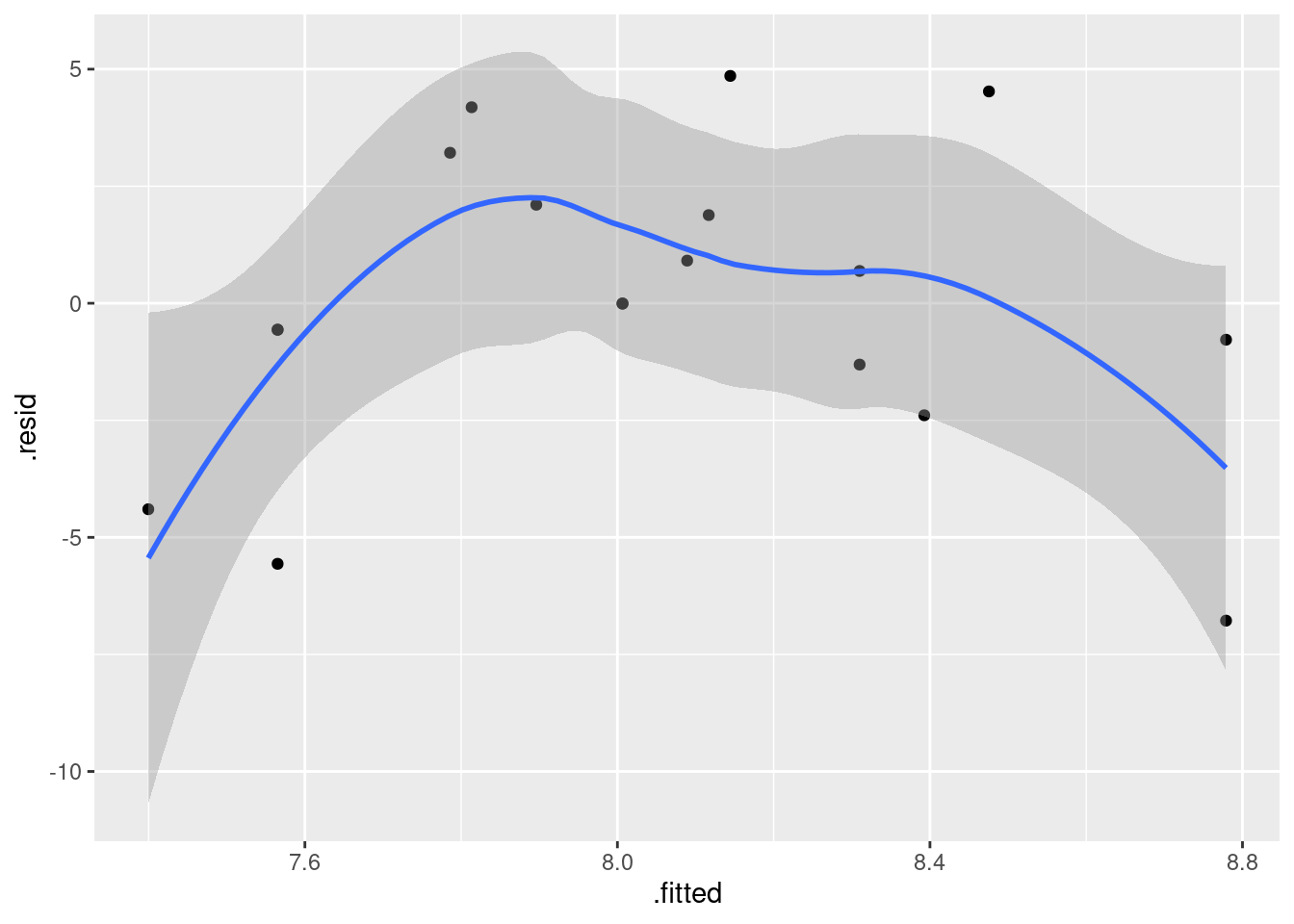

I intended that (i) should just be a matter of looking at residuals vs. fitted values:

There is no appreciable pattern on here, so no evidence of a curve (or apparently of any other problems).

Extra: you might read this that we should check residuals against the

\(x\)-variables as well, which is a similar trick to the above one for

plotting response against each of the explanatories. There is one step

first, though: use augment from broom first to get a

dataframe with the original \(x\)-variables and the residuals in

it. The following thus looks rather complicated, and if it confuses

you, run the code a piece at a time to see what it’s doing:

salaries.1 %>%

augment(salaries) %>%

pivot_longer(workqual:pubsucc, names_to="xname", values_to="x") %>%

ggplot(aes(x = x, y = .resid)) + geom_point() +

facet_wrap(~xname, scales = "free", ncol = 2)

These three residual plots are also pretty much textbook random, so no problems here either.

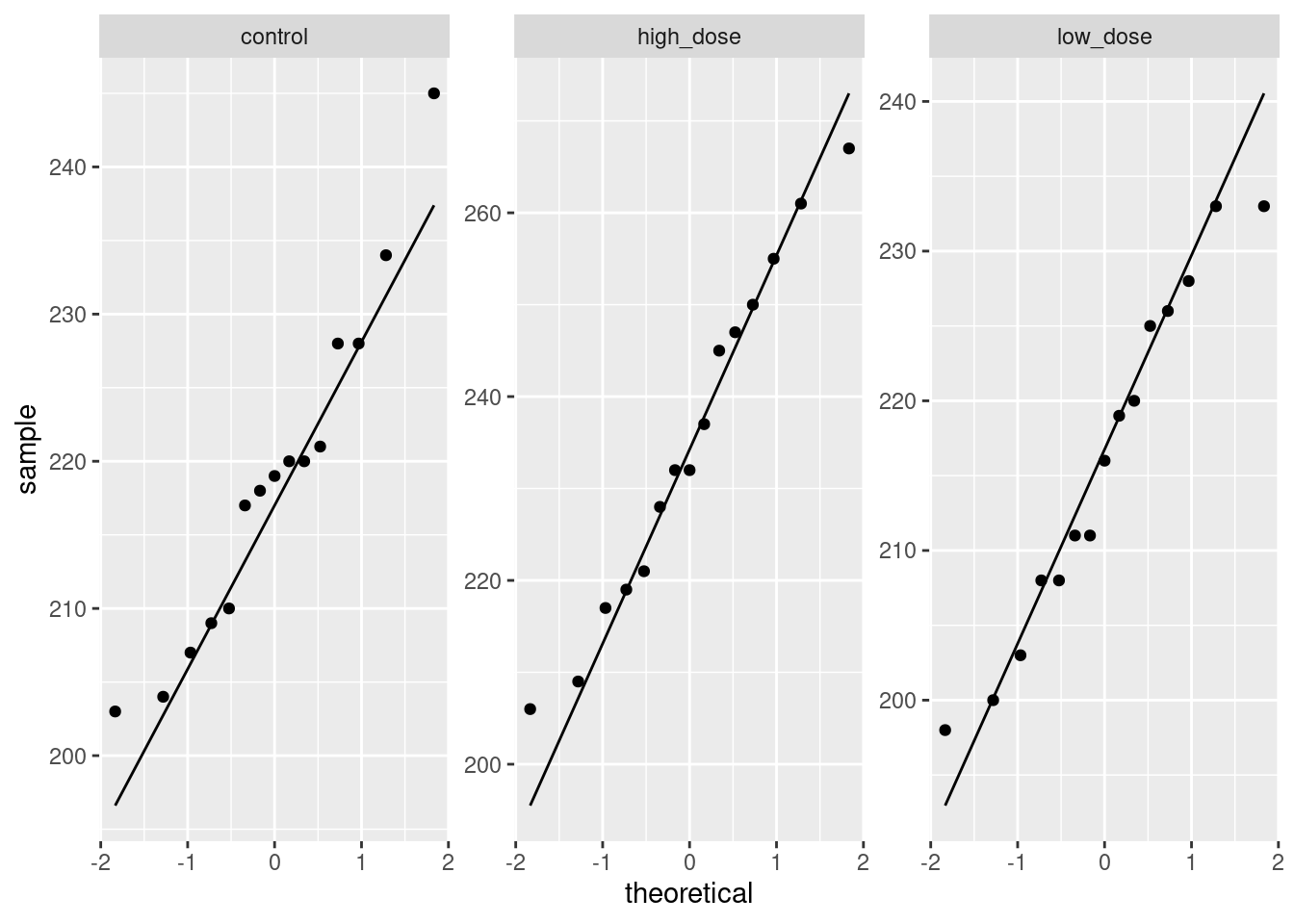

For (ii), look at a normal quantile plot of the residuals, which is not as difficult as the plot I just did:

That is really pretty good. Maybe the second smallest point is a bit far off the line, but otherwise there’s nothing to worry about. A quick place to look for problems is the extreme observations, and the largest and smallest residuals are almost exactly the size we’d expect them to be.

Our graph for assessing fan-in or fan-out is to plot the absolute values of the residuals against the fitted values. The plot from (i) suggests that we won’t have any problems here, but to investigate:

## `geom_smooth()` using method = 'loess' and formula 'y ~ x'

This is pretty nearly straight across. You might think it increases a bit at the beginning, but most of the evidence for that comes from the one observation with fitted value near 30 that happens to have a residual near zero. Conclusions based on one observation are not to be trusted! In summary, I’m happy with this linear multiple regression, and I don’t see any need to do anything more with it. I am, however, willing to have some sympathy with opinions that differ from mine, if they are supported by those graphs above.

17.4 Predicting GPA of computer science students

The file link contains some measurements of academic achievement for a number of university students studying computer science:

High school grade point average

Math SAT score

Verbal SAT score

Computer Science grade point average

Overall university grade point average.

- Read in the data and display it (or at least the first ten lines).

Solution

The usual:

##

## ── Column specification ─────────────────────────────────────

## cols(

## high_GPA = col_double(),

## math_SAT = col_double(),

## verb_SAT = col_double(),

## comp_GPA = col_double(),

## univ_GPA = col_double()

## )Two SAT scores and three GPAs, as promised.

- * Make a scatterplot of high school GPA against university GPA. Which variable should be the response and which explanatory? Explain briefly. Add a smooth trend to your plot.

Solution

High school comes before university, so high school should be explanatory and university should be the response. (High school grades are used as an admission criterion to university, so we would hope they would have some predictive value.)

## `geom_smooth()` using method = 'loess' and formula 'y ~ x'

- Describe any relationship on your scatterplot: its direction, its strength and its shape. Justify your description briefly.

Solution

Taking these points one at a time:

direction: upward (a higher high-school GPA generally goes with a higher university GPA as well. Or you can say that the lowest high-school GPAs go with the lowest university GPAs, and high with high, at least most of the time).

strength: something like moderately strong, since while the trend is upward, there is quite a lot of scatter. (This is a judgement call: something that indicates that you are basing your description on something reasonable is fine.)

shape: I’d call this “approximately linear” since there is no clear curve here. The smooth trend wiggles a bit, but not enough to make me doubt a straight line.

Looking ahead, I also notice that when high-school GPA is high, university GPA is also consistently high, but when high-school GPA is low, the university GPA is sometimes low and sometimes high, a lot more variable. (This suggests problems with fan-in later.) In a practical sense, what this seems to show is that people who do well at university usually did well in high-school as well, but sometimes their high-school grades were not that good. This is especially true for people with university GPAs around 3.25.

- * Fit a linear regression for predicting university GPA from high-school GPA and display the results.

Solution

Just this, therefore:

##

## Call:

## lm(formula = univ_GPA ~ high_GPA, data = gpa)

##

## Residuals:

## Min 1Q Median 3Q Max

## -0.69040 -0.11922 0.03274 0.17397 0.91278

##

## Coefficients:

## Estimate Std. Error t value Pr(>|t|)

## (Intercept) 1.09682 0.16663 6.583 1.98e-09 ***

## high_GPA 0.67483 0.05342 12.632 < 2e-16 ***

## ---

## Signif. codes:

## 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

##

## Residual standard error: 0.2814 on 103 degrees of freedom

## Multiple R-squared: 0.6077, Adjusted R-squared: 0.6039

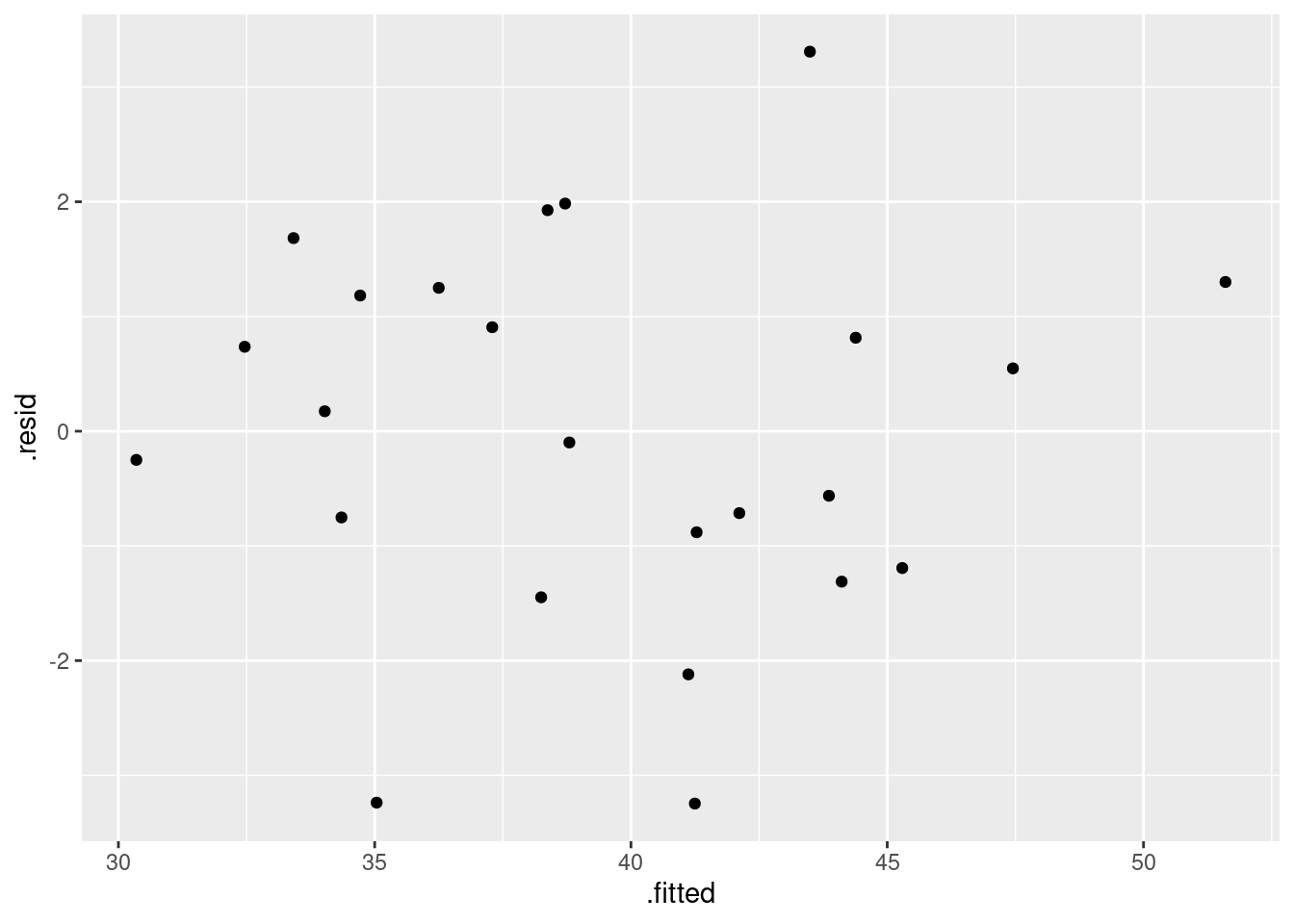

## F-statistic: 159.6 on 1 and 103 DF, p-value: < 2.2e-16Extra: this question goes on too long, so I didn’t ask you to look at the residuals from this model, but my comments earlier suggested that we might have had some problems with fanning-in (the variability of predictions getting less as the high-school GPA increases). In case you are interested, I’ll look at this here. First, residuals against fitted values:

## `geom_smooth()` using method = 'loess' and formula 'y ~ x'

Is that evidence of a trend in the residuals? Dunno. I’m inclined to call this an “inconsequential wiggle” and say it’s OK. Note that the grey envelope includes zero all the way across.

Normal quantile plot of residuals:

A somewhat long-tailed distribution: compared to a normal distribution, the residuals are a bit too big in size, both on the positive and negative end.

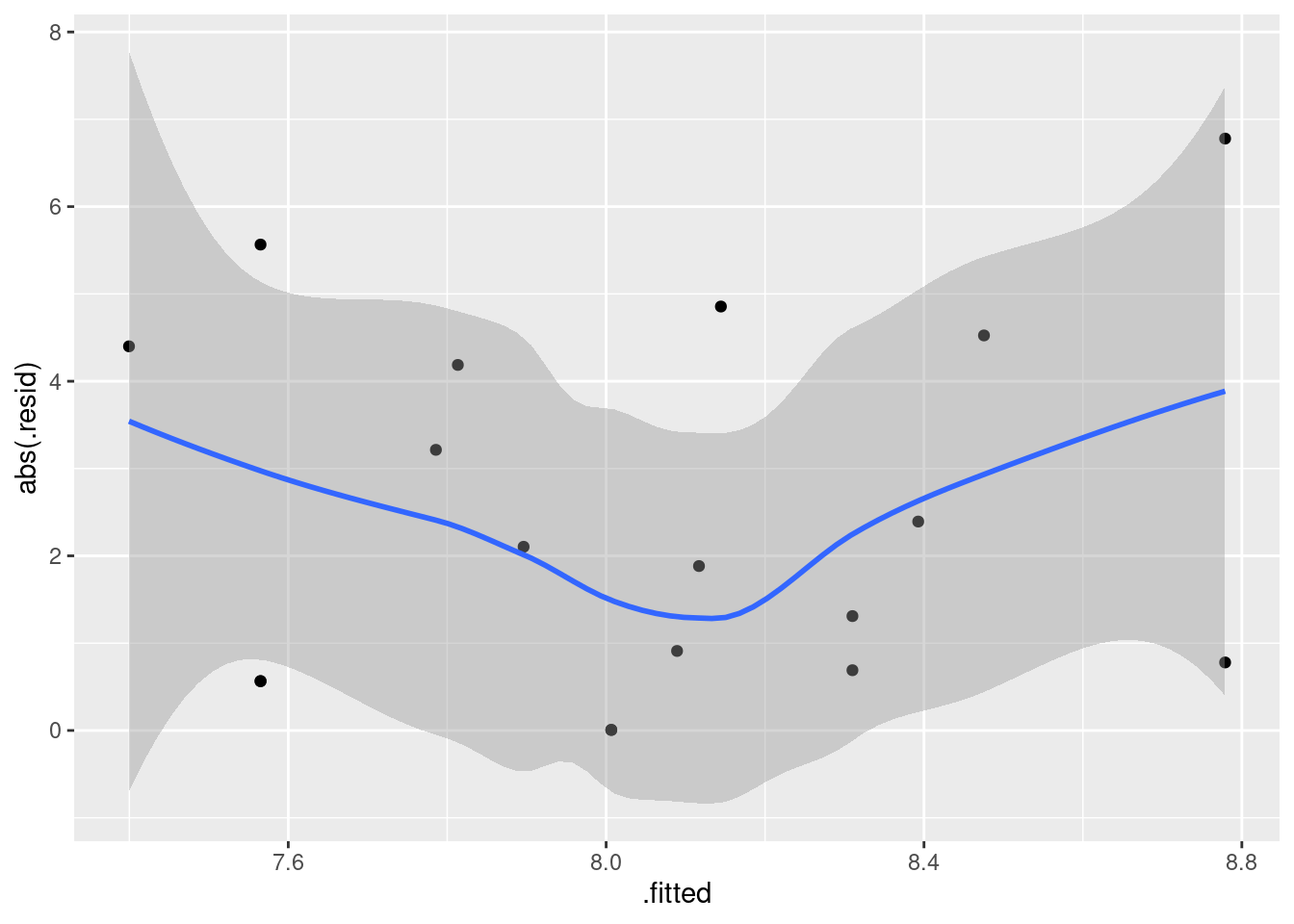

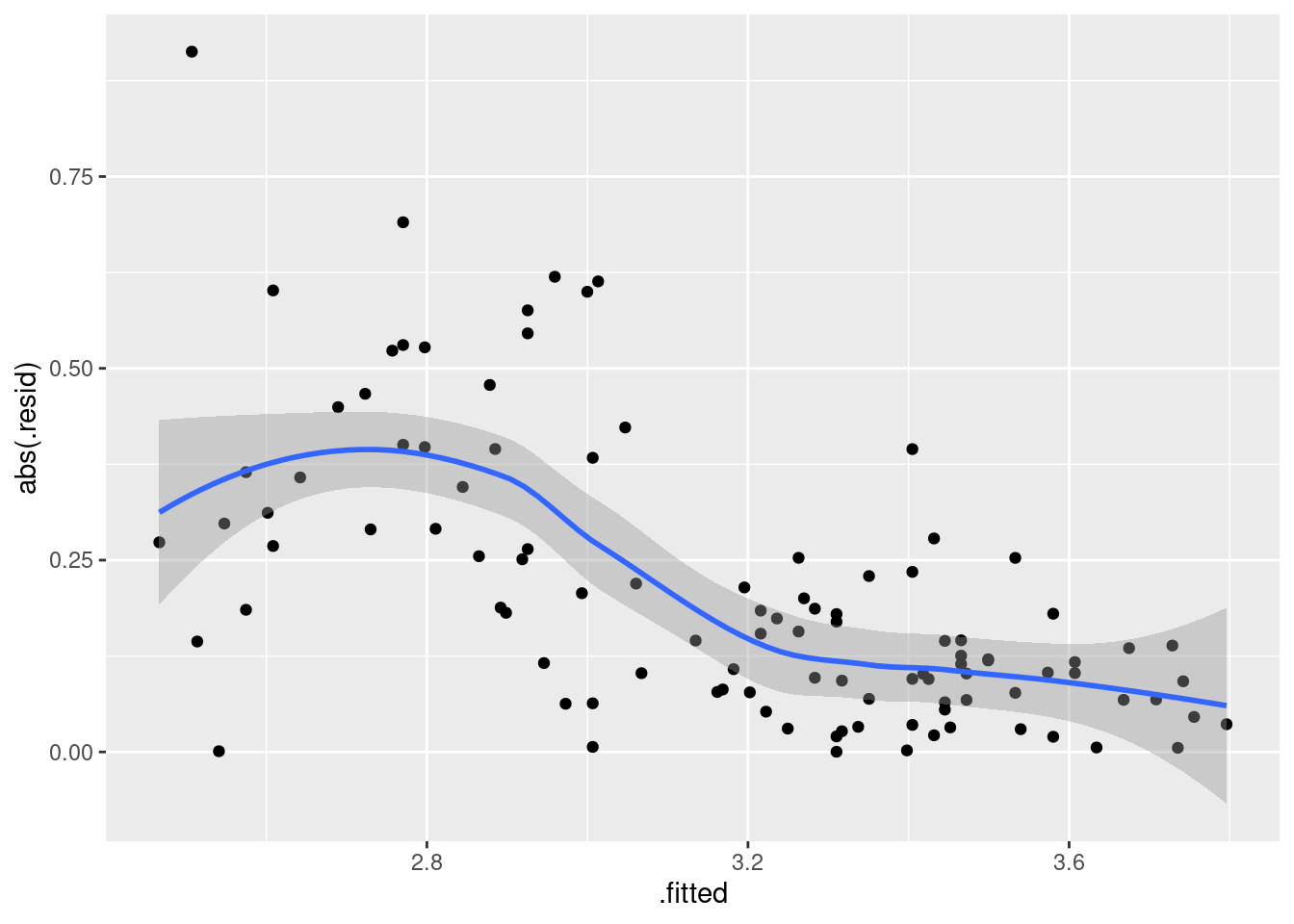

The problem I was really worried about was the potential of fanning-in, which we can assess by looking at the absolute residuals:

## `geom_smooth()` using method = 'loess' and formula 'y ~ x'

That is definitely a downward trend in the size of the residuals, and I think I was right to be worried before. The residuals should be of similar size all the way across.

The usual problem of this kind is fanning-out, where the residuals get bigger in size as the fitted values increase. The bigger values equals more spread is the kind of thing that a transformation like taking logs will handle: the bigger values are all brought downwards, so they will be both smaller and less variable than they were. This one, though, goes the other way, so the only kind of transformation that might help is one at the other end of the scale (think of the Box-Cox lambda scale), something like maybe reciprocal, \(\lambda=-1\) maybe.

The other thought I had was that there is this kind of break around a high-school GPA of 3 (go back to the scatterplot of (here)): when the high-school GPA is higher than 3, the university GPA is very consistent (and shows a clear upward trend), but when the high-school GPA is less than 3, the university GPA is very variable and there doesn’t seem to be any trend at all. So maybe two separate analyses would be the way to go.

All right, how does Box-Cox work out here, if at all?

It doesn’t. All right, that answers that question.

When I loaded MASS, I also loaded its select

function,

That is what that masked message above was about. and I might want to use the

tidyverse select

function later, and things could get confused. So let’s “unload”

MASS now:

## Warning: 'MASS' namespace cannot be unloaded:

## namespace 'MASS' is imported by 'PMCMRplus', 'lme4' so cannot be unloaded- Two students have been admitted to university. One has

a high school GPA of 3.0 and the other a high school GPA of

3.5. Obtain suitable intervals that summarize the GPAs that each of these two students might obtain in university.

Solution

Since we are talking about individual students, rather than

the mean of all students with these GPAs, prediction

intervals are called for. The first step is to make a data

frame to predict from. This has to contain columns for all the

explanatory variables, just high_GPA in this case:

and then feed that into predict:

## fit lwr upr

## 1 3.121313 2.560424 3.682202

## 2 3.458728 2.896105 4.021351and display that side by side with the values it was predicted from:

or this way, if you like it better:

Thus the predicted university GPA for the student with high school GPA 3.0 is between 2.6 and 3.7, and for the student with high school GPA 3.5 is between 2.9 and 4.0. (I think this is a good number of decimals to give, but in any case, you should actually say what the intervals are.)

I observe that these intervals are almost exactly the same length. This surprises me a bit, since I would have said that 3.0 is close to the average high-school GPA and 3.5 is noticeably higher. If that’s the case, the prediction interval for 3.5 should be longer (since there is less “nearby data”). Was I right about that?

gpa %>% summarize(

mean = mean(high_GPA),

med = median(high_GPA),

q1 = quantile(high_GPA, 0.25),

q3 = quantile(high_GPA, 0.75)

)More or less: the mean is close to 3, and 3.5 is close to the third quartile. So the thing about the length of the prediction interval is a bit of a mystery. Maybe it works better for the confidence interval for the mean:

These intervals are a lot shorter, since we are talking about all students with the high-school GPAs in question, and we therefore no longer have to worry about variation from student to student (which is considerable). But my supposition about length is now correct: the interval for 3.5, which is further from the mean, is a little longer than the interval for 3.0. Thinking about it, it seems that the individual-to-individual variation, which is large, is dominating things for our prediction interval above.

- * Now obtain a regression predicting university GPA from high-school GPA as well as the two SAT scores. Display your results.

Solution

Create a new regression with all the explanatory variables you want in it:

##

## Call:

## lm(formula = univ_GPA ~ high_GPA + math_SAT + verb_SAT, data = gpa)

##

## Residuals:

## Min 1Q Median 3Q Max

## -0.68186 -0.13189 0.01289 0.16186 0.93994

##

## Coefficients:

## Estimate Std. Error t value Pr(>|t|)

## (Intercept) 0.5793478 0.3422627 1.693 0.0936 .

## high_GPA 0.5454213 0.0850265 6.415 4.6e-09 ***

## math_SAT 0.0004893 0.0010215 0.479 0.6330

## verb_SAT 0.0010202 0.0008123 1.256 0.2120

## ---

## Signif. codes:

## 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

##

## Residual standard error: 0.2784 on 101 degrees of freedom

## Multiple R-squared: 0.6236, Adjusted R-squared: 0.6124

## F-statistic: 55.77 on 3 and 101 DF, p-value: < 2.2e-16- Test whether adding the two SAT scores has improved the prediction of university GPA. What do you conclude?

Solution

Since we added two explanatory variables, the \(t\)-tests in

gpa.2 don’t apply (they tell us whether we can take out

one \(x\)-variable). We might have some suspicions, but that’s

all they are. So we have to do anova:

If you put the models the other way around, you’ll get a negative \(F\)-statistic and degrees of freedom, which doesn’t make much sense (although the test will still work).

The null hypothesis here is that the two models fit equally well. Since the P-value is not small, we do not reject that null hypothesis, and therefore we conclude that the two models do fit equally well, and therefore we prefer the smaller one, the one that predicts university GPA from just high-school GPA. (Or, equivalently, we conclude that those two SAT scores don’t add anything to the prediction of how well a student will do at university, once you know their high-school GPA.)

This might surprise you, given what the SATs are supposed to be for. But that’s what the data say.

- Carry out a backward elimination starting out from your model in part (here). Which model do you end up with? Is it the same model as you fit in (here)?

Solution

In the model of (here), math_SAT was the

least significant, so that comes out first. (I use

update but I’m not insisting that you do:)

##

## Call:

## lm(formula = univ_GPA ~ high_GPA + verb_SAT, data = gpa)

##

## Residuals:

## Min 1Q Median 3Q Max

## -0.68430 -0.11268 0.01802 0.14901 0.95239

##

## Coefficients:

## Estimate Std. Error t value Pr(>|t|)

## (Intercept) 0.6838723 0.2626724 2.604 0.0106 *

## high_GPA 0.5628331 0.0765729 7.350 5.07e-11 ***

## verb_SAT 0.0012654 0.0006283 2.014 0.0466 *

## ---

## Signif. codes:

## 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

##

## Residual standard error: 0.2774 on 102 degrees of freedom

## Multiple R-squared: 0.6227, Adjusted R-squared: 0.6153

## F-statistic: 84.18 on 2 and 102 DF, p-value: < 2.2e-16Here is where we have to stop, since both high-school GPA and

verbal SAT score are significant, and so taking either of them

out would be a bad idea.

This is a different model than the one of

(here). This is the case, even though the model

with high-school GPA only was not significantly worse than the

model containing everything. (This goes to show that

model-building doesn’t always have nice clear answers.)

In the model I called gpa.2, neither of the SAT

scores were anywhere near significant (considered singly), but

as soon as we took out one of the SAT scores (my model

gpa.3), the other one became significant. This goes

to show that you shouldn’t take out more than one explanatory

variable based on the results of the \(t\)-tests, and even if

you test to see whether you should have taken out both of the SAT,

you won’t necessarily get consistent

results. Admittedly, it’s a close decision whether to

keep or remove verb_SAT, since its P-value is

close to 0.05.

The other way of tackling this one is via step, which

does the backward elimination for you (not that it was much

work here):

## Start: AIC=-264.6

## univ_GPA ~ high_GPA + math_SAT + verb_SAT

##

## Df Sum of Sq RSS AIC F value Pr(>F)

## - math_SAT 1 0.0178 7.8466 -266.36 0.2294 0.633

## - verb_SAT 1 0.1223 7.9511 -264.97 1.5777 0.212

## <none> 7.8288 -264.60

## - high_GPA 1 3.1896 11.0184 -230.71 41.1486 4.601e-09

##

## - math_SAT

## - verb_SAT

## <none>

## - high_GPA ***

## ---

## Signif. codes:

## 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

##

## Step: AIC=-266.36

## univ_GPA ~ high_GPA + verb_SAT

##

## Df Sum of Sq RSS AIC F value Pr(>F)

## <none> 7.8466 -266.36

## - verb_SAT 1 0.3121 8.1587 -264.26 4.0571 0.04662

## - high_GPA 1 4.1562 12.0028 -223.73 54.0268 5.067e-11

##

## <none>

## - verb_SAT *

## - high_GPA ***

## ---

## Signif. codes:

## 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1##

## Call:

## lm(formula = univ_GPA ~ high_GPA + verb_SAT, data = gpa)

##

## Coefficients:

## (Intercept) high_GPA verb_SAT

## 0.683872 0.562833 0.001265This gives the same result as we did from our backward

elimination. The tables with AIC in them are each step of

the elimination, and the variable at the top is the one that comes out

next. (When <none> gets to the top, that’s when you stop.)

What happened is that the two SAT scores started off highest, but once

we removed math_SAT, verb_SAT jumped below

<none> and so the verbal SAT score had to stay.

Both the P-value and the AIC say that the decision about keeping or

removing verb_SAT is very close.

- These students were studying computer science at university. Do you find your backward-elimination result sensible or surprising, given this? Explain briefly.

Solution

I would expect computer science students to be strong students generally, good at math and possibly not so good with words. So it is not surprising that high-school GPA figures into the prediction, but I would expect math SAT score to have an impact also, and it does not. It is also rather surprising that verbal SAT score predicts success at university for these computer science students; you wouldn’t think that having better skills with words would be helpful. So I’m surprised. Here, I’m looking for some kind of discussion about what’s in the final backward-elimination model, and what you would expect to be true of computer science students. Let’s look at the final model from the backward elimination again:

##

## Call:

## lm(formula = univ_GPA ~ high_GPA + verb_SAT, data = gpa)

##

## Residuals:

## Min 1Q Median 3Q Max

## -0.68430 -0.11268 0.01802 0.14901 0.95239

##

## Coefficients:

## Estimate Std. Error t value Pr(>|t|)

## (Intercept) 0.6838723 0.2626724 2.604 0.0106 *

## high_GPA 0.5628331 0.0765729 7.350 5.07e-11 ***

## verb_SAT 0.0012654 0.0006283 2.014 0.0466 *

## ---

## Signif. codes:

## 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

##

## Residual standard error: 0.2774 on 102 degrees of freedom

## Multiple R-squared: 0.6227, Adjusted R-squared: 0.6153

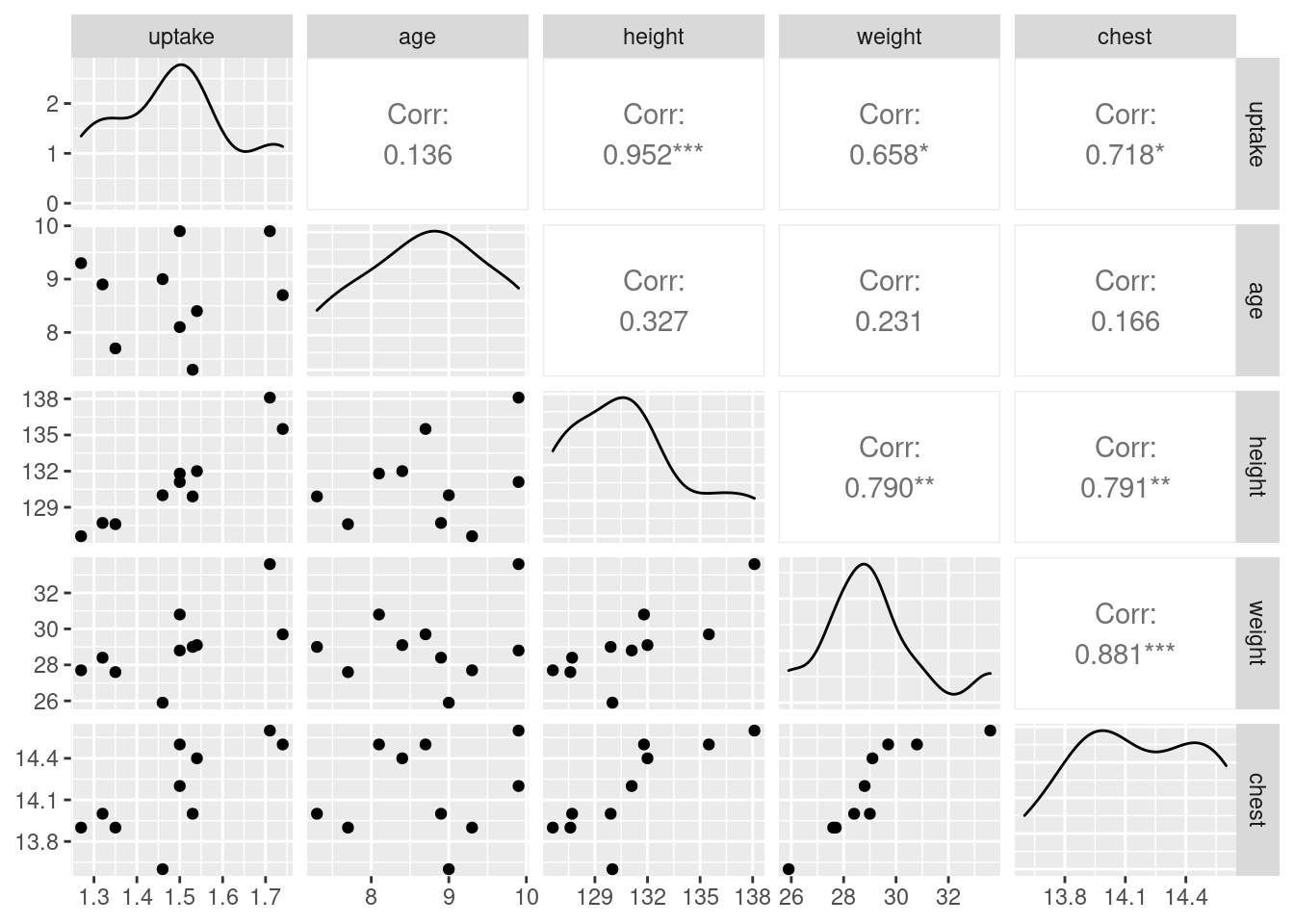

## F-statistic: 84.18 on 2 and 102 DF, p-value: < 2.2e-16The two slope estimates are both positive, meaning that, all else equal, a higher value for each explanatory variable goes with a higher university GPA. This indicates that a higher verbal SAT score goes with a higher university GPA: this is across all the university courses that a student takes, which you would expect to be math and computer science courses for a Comp Sci student, but might include a few electives or writing courses. Maybe what is happening is that the math SAT score is telling the same story as the high-school GPA for these students, and the verbal SAT score is saying something different. (For example, prospective computer science students are mostly likely to have high math SAT scores, so there’s not much information there.)

I think I need to look at the correlations:

## high_GPA math_SAT verb_SAT comp_GPA univ_GPA

## high_GPA 1.0000000 0.7681423 0.7261478 0.7914721 0.7795631

## math_SAT 0.7681423 1.0000000 0.8352272 0.6877209 0.6627837

## verb_SAT 0.7261478 0.8352272 1.0000000 0.6387512 0.6503012

## comp_GPA 0.7914721 0.6877209 0.6387512 1.0000000 0.9390459

## univ_GPA 0.7795631 0.6627837 0.6503012 0.9390459 1.0000000We’ll ignore comp_GPA (i) because we haven’t been thinking

about it and (ii) because it’s highly correlated with the university

GPA anyway. (There isn’t a sense that one of the two university GPAs

is explanatory and the other is a response, since students are taking

the courses that contribute to them at the same time.)

The highest correlation with university GPA of what remains is high-school GPA, so it’s not at all surprising that this features in all our regressions. The correlations between university GPA and the two SAT scores are about equal, so there appears to be no reason to favour one of the SAT scores over the other. But, the two SAT scores are highly correlated with each other (0.835), which suggests that if you have one, you don’t need the other, because they are telling more or less the same story.

That makes me wonder how a regression with the SAT math score and not the SAT verbal score would look:

##

## Call:

## lm(formula = univ_GPA ~ high_GPA + math_SAT, data = gpa)

##

## Residuals:

## Min 1Q Median 3Q Max

## -0.68079 -0.12264 0.00741 0.16579 0.90010

##

## Coefficients:

## Estimate Std. Error t value Pr(>|t|)

## (Intercept) 0.6072916 0.3425047 1.773 0.0792 .

## high_GPA 0.5710745 0.0827705 6.899 4.5e-10 ***

## math_SAT 0.0012980 0.0007954 1.632 0.1058

## ---

## Signif. codes:

## 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

##

## Residual standard error: 0.2792 on 102 degrees of freedom

## Multiple R-squared: 0.6177, Adjusted R-squared: 0.6102

## F-statistic: 82.4 on 2 and 102 DF, p-value: < 2.2e-16Math SAT does not quite significantly add anything to the prediction,

which confirms that we do better to use the verbal SAT score

(surprising though it seems). Though, the two regressions with the

single SAT scores, gpa.3 and gpa.4, have almost the

same R-squared values. It’s not clear-cut at all. In the end, you have

to make a call and stand by it.